TerraVest Industries (TVK.TO)

Note: I’m learning more about the company as I write this report, so feel free to leave any feedback on inaccuracies or additional information that I missed out on to improve the write-up. This company may be near the edge of my circle of competence – I’m in Singapore and the operations are mainly in Canada and the United States so I can’t see or verify things for myself, and much of what I know is what I’ve learned from trusted sources. However, I intend to learn more about TerraVest and its industry over time. I’m keen to hear any anti-thesis to this write-up so as to counteract any potential biases of mine.

I later turned the lessons from this research into a reusable blueprint for investment writeups.

Elevator Pitch

TerraVest is a small-cap, boring (and boring means unnoticed) company that takes excess cash flows from the company’s operations, carefully picks and acquires businesses at cheap valuations that offer synergies. It increases the price of the acquired company’s products and reduces the cost of production for both companies combined, all while maintaining or increasing demand for the combined products. The return on investment for each acquisition is therefore better than it initially appears, due to the synergies realised over time. Management’s track record suggests a continuation of successful acquisitions in the future.

The managers are disciplined capital allocators who are competent, think long-term, have great integrity, and are well-incentivized to create shareholder value (both CEO and CIO have the majority of their net worth in TerraVest stock). Management focuses on cash flows rather than accounting earnings and understands the importance of growing free cash flow and maintaining good returns on investments. Despite being a market leader in the industry it operates in, TerraVest remains a hidden gem, largely unnoticed by both institutional and retail investors, likely due to the lack of coverage by analysts.

Key Figures

- EV: CA$2,543.2M

- Insider Ownership: 21.1%

- P/FCF: 20.78x

- EV/NOPAT: 27.9x

- ROCE: 16.55%

- Rev 3yr CAGR: 43.67%

- NOPAT 3yr CAGR: 35.23%

- Gross Profit Margin 10yr CAGR: 2.05%

- Operating Margin 10yr CAGR: 0.08%

- Weighted Avg. Shares Outstanding Dil 10yr CAGR: -0.05%

Sourced from finchat.io, correct as of Dec 23rd, 2024. I might cherry-pick some numbers to fit the overall narrative (i.e., anomaly in the third-year number which makes CAGR calculation look bad). Verify the numbers yourself.

Introduction

Context 1: Propane industry

Propane is widely used in rural, off-grid areas where natural gas pipelines are unavailable. It is commonly used for heating (e.g., house heaters, cooking, temporary heating, etc.) due to several key advantages: ease of storage in liquid form, efficiency (high energy density per unit volume), and reliability regardless of weather conditions (e.g., batteries can fail in extreme cold). In short, propane offers reliability, efficiency, and portability for heating-related applications.

So how do we get propane? Propane is a byproduct of natural gas processing and extraction. Once the extraction process begins, it cannot be stopped without incurring significant costs, making it crucial to have sufficient storage capacity available to store the liquified propane. While the amount of propane in a well can be reasonably estimated, unexpected surpluses may still occur. When this happens, additional propane tanks must be sourced promptly to avoid disruptions (i.e., every bit of discarded propane is money wasted).

Transporting propane tanks can also pose logistical challenges, as extraction sites are typically in remote, off-grid locations. There are often limitations on the number of large vehicles capable of safely transporting pressurized propane tanks to and from these areas.

To streamline operations and reduce the administrative burden, it is essential to outsource the coordination of propane tank manufacturing, transport, and storage to a single company. A centralized approach provides a single point of contact, ensuring that the entire propane management process - from production to surplus handling - is efficiently resolved.

Picture this.

As a natural gas extractor, you need to store freshly extracted and processed propane and be fully prepared to manage unexpected surpluses beyond your initial estimates. A reliable partner offering end-to-end propane solutions - manufacturing, transport, and storage - will eliminate administrative and logistical headaches. This is where TerraVest comes in.

TerraVest Industries is a publicly traded company that owns a number of metal manufacturing businesses, including propane equipment such as large bulk storage, transport trailers, bobtails, crane service trucks, and more. TerraVest Industries is the parent company of TerraVest Tanks, Mississippi Tank Company, Signature Truck Systems, Pro-Par, Inc. and Maxfield – all long-term and stable companies with a reputation within the industry for producing high-quality units and having excellent customer service.

— TerraVest’s website

When analysing a company, it’s crucial to assess whether it still has potential for growth. TerraVest operates in an industry that is experiencing a gradual slowdown. As the next generation becomes increasingly environmentally conscious and governments advocate for sustainable energy solutions, natural gas usage is expected to decline over time.

However, this transition is likely to be slow due to the significant infrastructure investments and extended timelines required to shift to more sustainable energy sources.

In such scenarios, similar to the dynamics of a game like Snake.io, the playing field doesn’t necessarily need to keep expanding. The natural gas industry serves as a parallel example. While the overall market may not be growing significantly - largely due to environmental considerations favouring cleaner, more sustainable energy sources - a skillful player can still “gobble up” competitors and achieve growth.

For TerraVest, this situation presents a unique opportunity. The industry’s sluggish growth and general pessimism deter new entrants, reducing competitive pressures. This environment enables TerraVest to continue expanding through strategic acquisitions, allowing it to strengthen its position and capitalise on consolidation opportunities within the industry.

Some may be concerned with investing in a company that’s in a slowing industry (i.e., the propane market). Those are valid concerns. The energy transition may be pressing on propane’s (very) long-term growth, but the near- to medium-term reality is that many rural and industrial consumers remain highly dependent on propane for essential services. Until cost-effective, reliable, and widely distributed alternatives are fully deployed, propane usage is likely to continue. This transitional period could last for years, if not decades, especially in rural locations or specific industrial applications that currently lack a feasible alternative. Time is required to set up natural gas pipelines or electricity lines to rural households.

Others may also be concerned that companies in a slowing industry have to fight over a pie that’s not growing as fast as before. That will be a concern if, bringing back the Snake.io analogy, TerraVest wasn’t busy gobbling up other smaller companies like the big snake in Snake.io. TerraVest is well positioned - with its current size and competent managers - to continue its rate of growth.

On second thought, snakes usually have a negative connotation, so this probably isn’t my best analogy when I’m trying to preach about the goodness of TerraVest.

Context 2: A family-owned business in the propane industry

Suppose you are the owner of a small, family-owned propane tank manufacturer. You’re in your 50s, and seeing how this industry is not as exciting as others like in technology or Artificial Intelligence, your children are reluctant to take over the company. Being a small company means that you cannot hold too much inventory without incurring significant working capital, but this also means you need a longer lead time for storage tank orders. You notice this company TerraVest getting bigger every year through acquisitions, and despite setting higher prices, they are able to steal some of your customers due to their larger inventory which allows them to respond more readily to demand. You want to retire, your children don’t want to take over, your company’s growth potential has plateaued, and you’re looking to cash in and enjoy the rest of your life. Your company’s too small and the industry too unattractive (i.e., slowing growth) to gain the interest of private equity firms, and you want to entrust your life’s work to a buyer who knows the industry and will ensure the continuation of what you’ve built.

You set up a call with TerraVest because they are interested in acquiring your company, but they are stingy with the amount that they’ll pay up – below what you think your company is worth. However, with no better option, your desire to exit leads you to accept the deal anyway.

Industrial acquisitions, when done well (i.e., attractively priced, high ROI, synergistic relationship), can generate significant dividends long into the future, especially for companies that are able to leverage economies of scale (i.e., high fixed costs). Instead of competing against each other for resources and customers, acquisitions turn rivals into partners, and everyone wins more in the end with this collaboration. This can be likened to globalization, where countries focus on their competitive advantages, which in turn brings them more benefits than they would have as competitors.

Through disciplined (i.e., only purchase when the expected ROI is above the hurdle rate) acquisitions, TerraVest is able to buy unpolished gems at discounted valuations, which has allowed it to compound total shareholder returns (TSR) at roughly 30% CAGR.

Company Operations

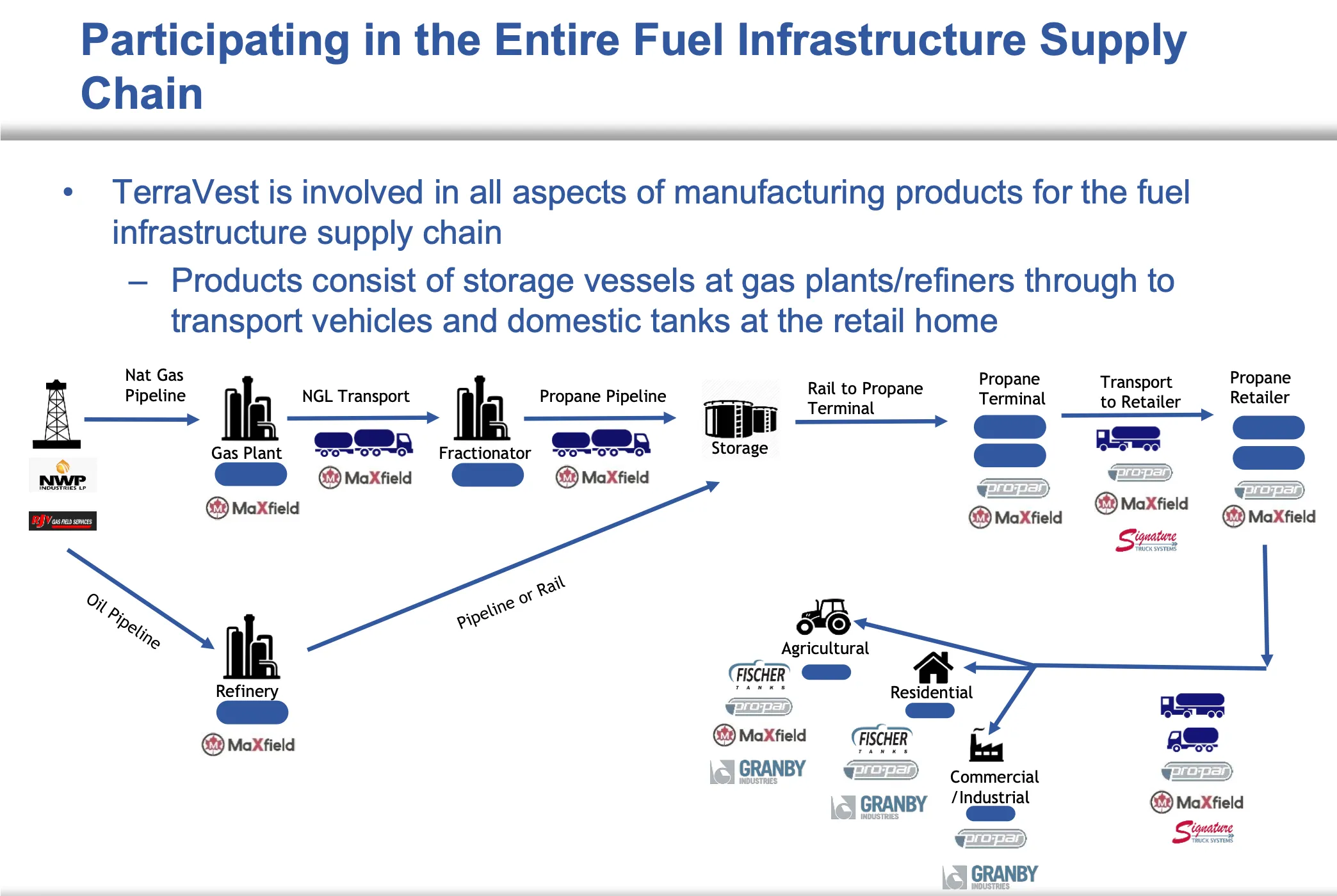

TerraVest is vertically integrated across the entire natural gas process, from extraction to sale to end-market users. It’s best summarised by the following graphic:

Figure 1: 2019 Investor's Presentation, TerraVest’s Operations

- TerraVest identifies family-owned / distressed businesses in this entire stack that are looking to exit and acquires them at cheap valuations while bringing profitable synergies to TerraVest’s entire operation. TerraVest says in its press releases that it “is focused on acquiring and operating market-leading businesses that will benefit from TerraVest’s financial and operational support.” They have proven to be hugely successful and disciplined (i.e., not overpaying) in this regard. - TerraVest is a “market-leading manufacturer of home heating products, propane, anhydrous ammonia (“NH3”) and natural gas liquids (“NGL”) transport vehicles and storage vessels, energy processing equipment and fiberglass storage tanks” in resource-rich Canada and America. - More in-depth details of the company’s specific operations are outlined by the many fantastic write-ups attached in the Resources section.Competitive Advantage / Moat

Figure 2: 2019 Investor's Presentation, Acquisition Record

As illustrated in Figure 1, a large part of TerraVest’s operations relies on steel. A key benefit of TerraVest over their smaller competitors (aka acquisition targets) is their ability to go direct to steel mills and gain a bulk discount on the cost of steel. By contrast, smaller companies often have to buy supplies from middlemen who are parasites on the smaller company’s profits. Their direct access to steel mills becomes a key competitive advantage / moat that will only strengthen as they grow bigger through acquisitions (i.e., leverage greater economies of scale to gain further discounts or maximise utilisation rates of equipment; see Figure 2).

I believe that the company, under the leadership of CEO Dustin Haw and his CIO Mitchell Gilbert, will continue making strategic and successful acquisitions which they’ve proven themselves capable of in the last decade. The two of them work hand-in-hand; Gilbert finds companies to acquire, while Haw spends his time optimising and restructuring the acquired companies to maximise the synergies with existing operations while improving their margins.

Figure 3: 2019 Investor's Presentation, Organic Growth

TerraVest’s acquisition skills give it another key advantage in continuing to grow in a slowing industry. While organic growth is hindered due to the nature of the industry, TerraVest’s growth-by-acquisition strategy, coupled with its ability to identify attractive acquisition targets at cheap valuations allows them to flourish where others wither. Nevertheless, TerraVest continues to invest in its core business for increased capital efficiencies and productivity gains to boost organic growth.

Valuation

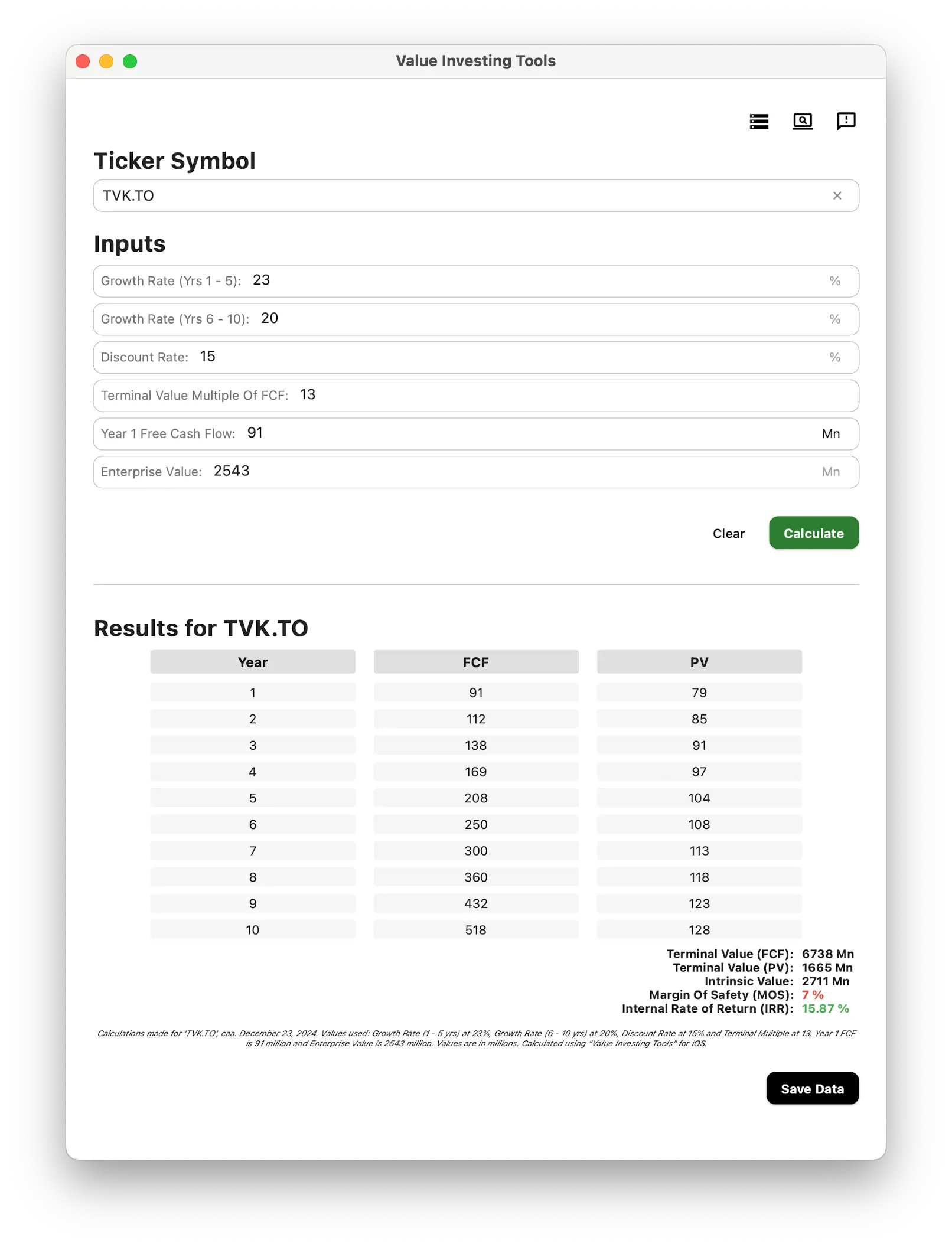

I’m not confident in my valuation abilities at the moment, and instead of pretending that I know how to value it well, I’ll rely on valuations done by superior / more experienced investors, which you can find in the Resources section. Nevertheless, here’s a simple back-of-the-envelope calculation using past growth rates (caution! Past results do not reflect future performance. This assumes the company continues to operate and finds great opportunities as it did before, ceteris paribus).

Figure 4: Value Investing Tools

“Growth Rate” refers to the projected NOPAT growth rate and I’m using NOPAT as a substitute for FCF. TerraVest has seen an increase in NOPAT growth rate in the last decade. As the company grows bigger, the benefits it gains from its suppliers should increase (i.e., leveraging larger economies of scale).

However, as an acquirer grows, the size and number of acquisitions will have to increase as well to maintain the same growth rate. This may prove to be a challenge for management as they have to keep finding attractive acquisition targets. However, TerraVest usually finds 1-2 acquisitions per year and has hundreds on its list of acquisition targets. Their ability to buy more of these companies at discounted valuations when times are bad provides a natural hedge to the company. This downside of having to grow through acquisition is also countered by management’s push to improve margins and capital efficiencies within the company.

I have factored this in by reflecting a decrease in growth rate from the current NOPAT 3yr CAGR of 35% to 23% for the first 5 years, and then 20% for the final 5 years in this 10-year projection. I have also chosen a terminal EV/NOPAT multiple of 13x, a contraction from the current 27.9x as more of the company’s potential gets realised over time.

The discount rate reflects my opportunity cost of investing in TerraVest. Some use the risk-free rate for this, but I’m using the yearly target returns of my portfolio at 15%. The results of this (probably inaccurate) valuation model reflect an IRR of 15.87%, which implies that we could expect the company to generate returns for us at a compounded rate of 15.87% should the assumptions hold true, at the current price.

Note: Discounted Cash Flow analysis could be a misleading indicator as growth rates and multiples can be toyed with to achieve the “value” that the investor wants to see, in line with his beliefs of the company’s trajectory. I may be subjected to this bias, so I’ll still urge the reader to refer to the valuations made by professional investors in the Resources section.

Potential Downsides

- Cyclicality: The oil and gas industry experiences business cycles. This can be due to geopolitical situations, technological advancements (i.e., high energy consumption by large language models), or economic growth where positive outlook drives higher production. Consequently, TerraVest operates in a cyclical industry which some investors may find unattractive. However, as Chris Waller from Plural Investing aptly points out, TerraVest can turn down-cycles into highly beneficial situations by using the excess cash flows generated from the core business to acquire more businesses at significantly discounted valuations (i.e., due to an increase in distressed companies). This is likened to a shrewd investor going shopping when the market is in a cyclical downturn and multiples are temporarily compressed. It can also be noted that the downside is padded as heating is an essential utility, so the company won’t be irrelevant overnight. The company has also proven its ability to buy back shares aggressively when it judged the price to be undervalued, which it has demonstrated in 2012 when it repurchased 36% of its shares.

- Bad Acquisitions: Most acquisitions for most companies do not work out. This has led prominent investors like Peter Lynch to coin the term “Diworsification”. TerraVest’s management has so far proven themselves to be shrewd, successful acquirers which makes them a minority in the business world. But this could change. If management starts making poor acquisitions (i.e., lowering their hurdle rate, purchasing companies for the sake of it without many synergies with existing operations, paying excessive prices for mediocre businesses), and since their acquisition skills are a key attraction of TerraVest, we should be looking to exit the company.

- Key Man Risk: TerraVest before CEO Dustin Haw is a very different company. Haw’s growth-by-acquisition and restructuring strategy is what makes TerraVest appealing today. Over the past 10 years, Haw, together with CIO Mitchell Gilbert, has worked to deliver 30% CAGR TSR. Both of them are Chartered Financial Analysts (CFA) and have great synergies with each other. Haw’s leadership is widely praised by those in close contact with him and his competence is evident in TerraVest’s results. The two of them are what make this investment attractive to me.

- Increased Recognition by Investors: In the last year alone, the stock has appreciated 182%, largely fuelled by a multiple expansion. The stock is no longer as cheap as it was before, and it currently trades at an EV/NOPAT of 27.9x. Investors have pulled forward future performance and priced in more of the company’s future cash flows. This implies a short-term downside risk when the momentum slows or when management disappoints with results below expectations.

Potential Upsides / Catalysts

- Maintain or accelerate acquisition pace of great and cheaply priced targets

- Increased investor attention on the business

- More favourable business environment under Trump’s administration

- Strategic share repurchases (i.e., only when share price is depressed / undervalued, no dilution to fund acquisition)

Resources

- https://finchat.io/

- https://mcusercontent.com/2511717cdf1bae9a0638c942a/files/d09e996a-6b1a-c4ce-a1d9-d510fa7b2d3d/Bonhoeffer_Partner_Letter_Q1_2023.pdf

- https://terravestindustries.com/

- https://terravestindustries.com/wp-content/uploads/2019/02/TerraVest-2019-Investor-Presentation-v3.pdf

- https://terravestlpg.com/

- https://www.fairwayresearch.com/p/terravest-industries

- https://www.pluralinvesting.com/research (This is a must-read, I first learned about TerraVest through this write-up by Chris Waller)

- https://podcasts.apple.com/sg/podcast/yet-another-value-podcast/id1526149547?i=1000649190578

- https://open.spotify.com/episode/6Lqojp4AqCJch2jDA4rr7z?si=7626d327329f4a31

Potential Edits / Refinements / Clarifications

- More detailed valuation model that factors in clearer insights into each of TerraVest’s business segments.

- Analysis of TerraVest’s competitors.

- Develop an anti-thesis to the investment thesis.

I’ll edit this article as I learn more about valuation / this company in the future.

Disclaimer: None of this is financial advice. I own shares in TerraVest Industries and I might be biased. I may also buy or sell shares in TerraVest Industries at any time. Please do your own due diligence before making any investment decisions.